Research Finder

Find by Keyword

Is Microsoft's AI Growth Sustainable, or Just an Early Surge?

Cloud revenue soars, AI demand explodes, but non-AI Azure struggles to keep pace.

Microsoft's AI-driven growth continues to dominate, with a $13 billion AI run rate (+175% YoY) fueling Azure’s 31% growth. However, the company's heavy AI infrastructure investments ($22.6B) are straining margins, and scaling challenges could slow momentum. While AI demand remains strong, Microsoft must address execution issues in its non-AI Azure business and find a sustainable balance between AI expansion and traditional cloud workloads to maintain long-term stability.

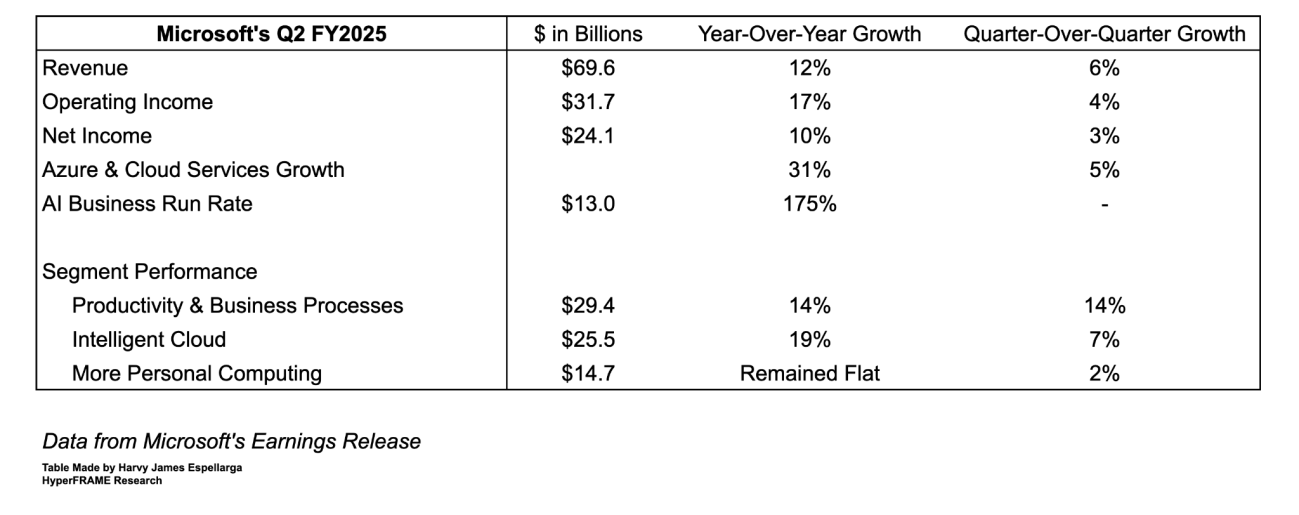

By the Numbers

- Revenue: $69.6 billion (+12% YoY, +6% QoQ)

- Operating Income: $31.7 billion (+17% YoY, +4% QoQ)

- Net Income: $24.1 billion (+10% YoY, +3% QoQ)

- Azure & Cloud Services Growth: +31% YoY, +5% QoQ

- AI Business Run Rate: $13 billion (+175% YoY)

- Segment Performance:

- Productivity & Business Processes: $29.4 billion (+14% YoY, +5% QoQ)

- Intelligent Cloud: $25.5 billion (+19% YoY, +7% QoQ)

- More Personal Computing: $14.7 billion (flat YoY, +2% QoQ)

Key Highlights

- Microsoft Cloud revenue surpassed $40 billion for the first time, driven by AI acceleration.

- AI-related services contributed 13 percentage points to Azure’s 31% growth, with OpenAI commitments fueling demand.

- Non-AI Azure growth remains challenged by execution issues, particularly in indirect sales channels.

- Microsoft 365 Copilot adoption exceeded expectations, with strong seat expansion and engagement growth.

- Capital expenditures remain high at $22.6 billion, as Microsoft scales AI infrastructure to meet demand.

The News:

Microsoft reported strong Q2 FY25 earnings, with revenue of $69.6 billion, up 12% year-over-year, and net income of $24.1 billion. The company’s AI-driven cloud strategy continues to pay off, with Azure AI services growing 157% YoY, contributing significantly to the company’s 21% Microsoft Cloud growth. However, the broader Azure business showed signs of execution challenges, particularly in non-AI-related cloud services. Meanwhile, Microsoft 365 Copilot adoption saw significant momentum, helping to drive higher-value commercial contracts. To read the full press release on Microsoft’s Q2 FY2025 earnings, please click this link.

Analyst Take

Based on what we are observing, Microsoft is firing on all cylinders when it comes to AI. The $13 billion AI run rate is simply astounding. But, and this is a big but, we are going to be tracking a few key things closely to see if this is truly sustainable.

First, can they keep up with demand? It's a land grab right now, and everyone wants the best AI tools. Microsoft is throwing billions at infrastructure, but even they are struggling to scale fast enough. If they can't deliver the compute power when and where it's needed, that incredible growth could hit a wall.

Second, how will they balance this AI-fueled expansion with the rest of their Azure business? It's great that AI is driving Azure growth, but they can't afford to neglect their core cloud offerings. We'll be watching closely to see how they address those execution challenges in the non-AI parts of Azure. My perspective is that long-term success hinges on a balanced portfolio.

Finally, Microsoft 365 Copilot is already proving to be a game-changer. The early adoption numbers are impressive, but the key question is monetization. Can they convert this initial growth into sustainable revenue growth? We will be tracking how Copilot impacts their pricing power and average revenue per user in the coming quarters.

Coming into 2025, Microsoft's results highlight a critical shift demonstrating that AI is no longer a sideshow, it's becoming the main event. But the transition won't be without its bumps. HyperFRAME will be closely monitoring how Microsoft navigates these challenges and how the company will capitalize on its market opportunities in the quarters to come.

Copilot, Copilot, and Copilot - What’s New?

The company’s AI business has reached a $13 billion annualized run rate, growing at an astonishing 175% YoY. This demand is largely fueled by strategic partnerships (notably OpenAI) and the rapid adoption of Copilot across Microsoft 365 and GitHub. Azure revenue grew by 31%, with 13 points of that growth coming directly from AI-related services. However, non-AI Azure workloads showed signs of stagnation due to shifting sales strategies and slower enterprise migrations.

Microsoft also provided insights into its ongoing AI infrastructure expansion, with capital expenditures reaching $22.6 billion this quarter. The company emphasized its investments in long-term AI infrastructure, balancing training and inference workloads while optimizing cost structures. Notably, it continues to integrate OpenAI’s advancements exclusively on Azure, further solidifying its cloud positioning.

AI Being A Game Changer, But Not Without Risks

AI is proving to be the single biggest driver of Microsoft's enterprise cloud expansion. The 175% YoY growth in AI revenue is unmatched in the industry, demonstrating enterprise-wide deployments beyond proof-of-concept stages. However, sustaining this pace will depend on several factors:

Compute Constraints: Microsoft is operating in a highly capacity-constrained environment. Azure AI growth outpaced expectations, but scaling AI infrastructure remains a major bottleneck. Put simply NVIDIA can only make so many GPU’s. While Microsoft has invested heavily in data centers and AI compute, meeting future demand will be a continuous challenge.We are seeing every HyperScaler focus on the AI build out, with Satya Nadella recently commenting that Microsoft is focused on its $80bn CapEx investments. This build out plan will be key if Microsoft is going to continue to lead in the AI infrastructure arms race.

Cost vs. Profitability: Scaling AI workloads is expensive. Despite strong revenue growth, AI-related infrastructure investments are putting pressure on Microsoft’s cloud gross margins. As inference costs decrease due to optimizations (e.g., DeepSeek’s innovations and software-driven efficiencies), Microsoft could see margin improvements—but in the short term, AI expansion remains capital-intensive.

Additional commentary on DeepSeek:We remain skeptical on the cost projections from DeepSeek on its cost to train the R model, however all the negative news/assumptions aside (and if all claims are true), it’s a great driver for innovation and cost-efficiency. If claims around it being created with a budget of $6 million, then we have two questions. First, are these claims legitimate? And second, are US companies going to pull a rabbit out of a hat with newer, better, and faster AI solutions? This is something we will be monitoring as this affected the market last Monday andwe believe that the sell-off was an overreaction to the announcements of DeepSeek.

Competitive Pressure: While OpenAI’s exclusive commitment to Azure gives Microsoft a competitive advantage, competitors like Google Cloud and AWS are aggressively scaling their own AI offerings. Also we are hearing that the OpenAI and Azure partnership is under review and that OpenA may have the ability to look at other providers such as Oracle for infrastructure. While this currently speculation, we will be tracking it closely as this develops. The long-term question is whether OpenAI’s models (and those from other partners) will continue to drive Azure’s leadership, or if customers will start demanding more model flexibility, particularly from open-source approaches, across clouds.

Non-AI Azure: A Slower Climb

While AI-related workloads drove significant growth, non-AI Azure services, including traditional cloud migrations and app hosting, did not meet expectations. Microsoft cited execution challenges in its “scale motions,” particularly among customers reached via indirect sales channels. This could be attributed to shifting customer priorities; as enterprises invest heavily in AI, they may be slowing other cloud transformation projects.

Microsoft’s response has been to refine its sales strategy, ensuring a balance between AI expansion and broader cloud adoption. But the broader takeaway is clear: Azure’s long-term growth cannot solely depend on AI, it must continue to capture traditional cloud workloads to maintain its overall trajectory.

Microsoft 365 Copilot: Still A Key Growth Driver

Copilot adoption continues to impress. Customers have increased seats by over 10x since launch, signaling strong demand for generative AI-driven workplace productivity. Importantly, engagement intensity is up 60% QoQ, suggesting that Copilot is delivering tangible value beyond initial adoption.

However, monetization remains an area to watch. While Copilot is contributing meaningfully to Microsoft 365's revenue growth, its long-term impact on enterprise pricing and ARPU (average revenue per user) will determine its ultimate success. If Microsoft can continue upselling Copilot while improving its pricing power, it could be one of the strongest AI-driven revenue levers in the coming years.

Looking Ahead

Based on what we observing, Microsoft’s AI-driven growth strategy is working, but sustaining it will require overcoming infrastructure constraints, margin pressures, and competitive challenges. The key trend we will be tracking is whether AI-related revenue can maintain its explosive trajectory as enterprise adoption matures.

Going forward, we will be looking for how Microsoft addresses Azure’s non-AI workload execution issues. If AI is driving most of the cloud growth, it raises questions about long-term sustainability once the current AI adoption wave normalizes. Additionally, Copilot’s continued expansion across Microsoft 365 and GitHub will be crucial in determining Microsoft’s ability to monetize AI at scale.

Microsoft’s Q2 results highlight a shift in enterprise cloud spending priorities, AI is now a primary driver, but traditional cloud workloads are facing new adoption headwinds. HyperFRAME will be closely monitoring how Microsoft manages this balance in future quarters.

Harvy James Espellarga | Analyst In Residence - FinOps and Earnings Coverage

Harvy James Espellarga is a financial analyst with a proven track record of analysing the financial performance of tech companies. He brings a deep understanding of accountancy principles and specializes in FinOps, helping organizations optimize their cloud spending and maximize ROI. His insightful analyses have been featured in publications like Seeking Alpha, where he provides expert commentary on performance and operational strategies for tech companies. He also previously contributed to cutting-edge research on emerging industry trends at The Futurum Group, supporting leading research directors.

Steven Dickens | CEO HyperFRAME Research

Regarded as a luminary at the intersection of technology and business transformation, Steven Dickens is the CEO and Principal Analyst at HyperFRAME Research.

Ranked consistently among the Top 10 Analysts by AR Insights and a contributor to Forbes, Steven's expert perspectives are sought after by tier one media outlets such as The Wall Street Journal and CNBC, and he is a regular on TV networks including the Schwab Network and Bloomberg.