Research Finder

Find by Keyword

Can Determinism Be Productized for the Software Defined Vehicle?

NXP and Quanta announce a turnkey stack spanning S32 compute, TSN switching, and middleware aiming to remove the validation labor that stalls zonal vehicle programs.

5/29/2026

Key Highlights

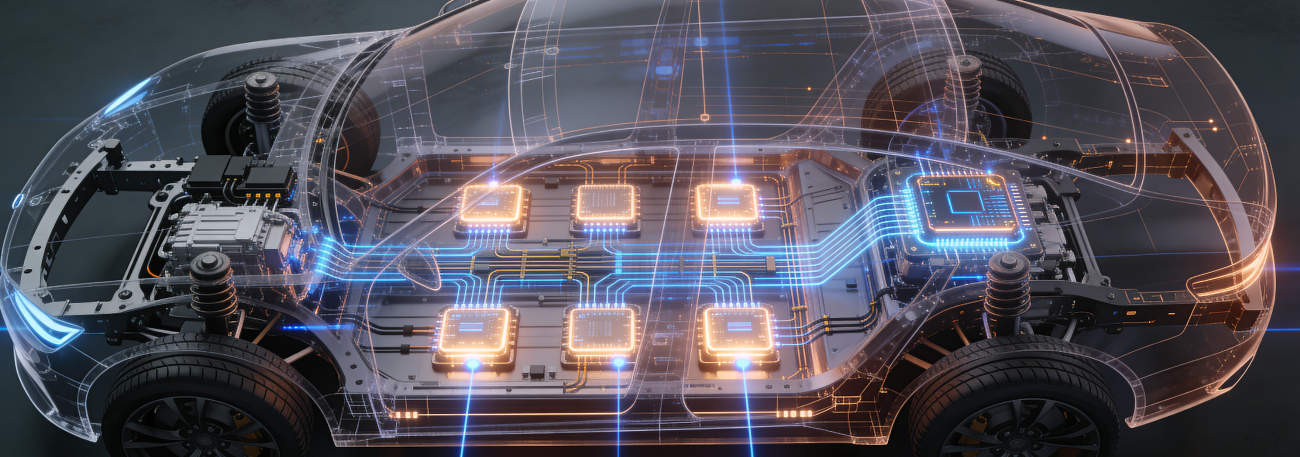

- NXP and Quanta are collaborating on a deterministic zonal networking solution for software defined vehicles, built on the NXP S32 automotive processing platform and TrustMotion MotionWise middleware.

- The solution is designed to deliver predictable end-to-end latency and low jitter across both vehicle compute hosts and in-vehicle networks, with the stated aim of reducing late-stage integration risk.

- Delivered as a single validated platform, it combines S32 zonal compute, SJA1110 TSN Ethernet switching, CAN and LIN connectivity, and multi-PMIC power management with automated topology discovery, schedule generation, and CI/CD deployment.

- The partners are working toward future alignment with the NXP CoreRide zonal reference system, with demonstrations underway on Quanta platforms and additional showcases planned through 2026.

- The choice of Quanta, a hyperscale server ODM rather than a traditional Tier 1 supplier, suggests the automotive supply chain is beginning to absorb data center integration practices, while NXP's framing reads as an attempt to reposition the zonal contest around integration risk rather than processor performance.

The News

NXP Semiconductors and Quanta have unveiled a deterministic zonal networking solution for software defined vehicles. The combined offering aims to deliver predictable, real-time communication across next generation vehicle networks by pairing NXP's S32 automotive processing platform with TrustMotion MotionWise middleware. The platform targets a persistent OEM pain point of ensuring deterministic timing across both compute hosts and network components. The companies say this pain point creates late-stage integration risk for OEMs facing a scattered set of offerings. The offering is to be delivered as a single validated stack spanning S32 zonal compute, SJA1110 TSN switching, CAN and LIN connectivity, and multi-PMIC power management. The supported modes include: automated topology discovery, schedule generation, and CI/CD deployment, with the partners signaling future alignment to the NXP CoreRide zonal reference system. The solution is available now to OEMs and ecosystem partners, with demonstrations underway on Quanta development platforms and additional showcases planned through 2026 (NXP newsroom).

Analyst Take

The most revealing detail in this announcement is the partnership. NXP is a storied company that posted $12.27 billion in 2025 revenue and sits among the top tier of automotive semiconductor suppliers. The partnership advances its zonal story alongside Quanta, a Taiwanese systems manufacturer best known for building servers for the world's hyperscalers rather than wiring harnesses for the world's automakers. That selection is a signal of thinking beyond traditional automotive. Here is our contrarian view: while much of the SDV conversation fixates on raw in-vehicle compute and TOPS counts, NXP and Quanta appear to be betting that the binding constraint on zonal programs is not horsepower at all, but deterministic timing and integration risk. The selection of Quanta reflects a broader shift in the automotive value chain, where OEMs are reaching deeper into the ecosystem to engage ODMs with data center networking expertise. This brings proven dynamic network configuration capabilities to the challenge of Ethernet consolidation and zonal coordination; expertise that has already been battle-tested at hyperscale. They are, in effect, attempting to productize determinism. If that thesis holds, the zonal contest may be decided less by who ships the fastest processor and more by who removes the most validation labor from the OEM.

What Was Announced

The solution is architected as a turnkey, validated platform versus a component bundle, which is the more consequential design choice. At the compute layer, S32 automotive processors provide what NXP describes as safe, secure, and OTA-ready zonal controllers. The networking layer is built on SJA1110 Time-Sensitive Networking switches, complemented by CAN and LIN connectivity and scalable multi-PMIC power management. Binding these together is TrustMotion's MotionWise middleware, split into MotionWise Schedule for deterministic scheduling and MotionWise Communication for the data path. The partners indicate that this should enable end-to-end determinism across both hosts and networks rather than leaving timing to be reconciled by the OEM late in development. Operationally, the platform is designed around a plug-and-play development flow that supports automated topology discovery, schedule generation, and deployment through a continuous integration workflow, with continuous optimization based on runtime data. Beyond the first implementation, the real multiplier lies in subsequent software updates. A deterministic middleware layer can compress integration and validation effort by nearly an order of magnitude on follow-on cycles, enabling the kind of scalable DevOps cadence that true SDV programs require rather than repeated try-and-error validation. NXP positions the result as predictable end-to-end latency and low jitter that protects system-level Quality of Service. The companies cite latency-sensitive use cases that suggest the intended breadth: audio over Ethernet, high-performance compute up-integration, real-time RCP control, and smart energy networking. Quanta contributes its Adaptive Zonal System for integration, validation, and deployment, and both sides indicate the work is aligning toward NXP's CoreRide zonal reference system, a pre-integrated reference design that ecosystem partners build against rather than assemble from scratch. We would read CoreRide alignment as the more strategic thread here. That a reference architecture is how a supplier converts a point solution into a repeatable program template with the aim of compounding as each added participant lowers the cost of the next integration.

Market Analysis

The competitive stakes scale with the category. The McKinsey Center for Future Mobility projects the global automotive software and electronics market reaching roughly $519 billion by 2035, growing well ahead of the roughly 1 percent annual pace of the overall vehicle market. That divergence helps explain why suppliers are racing to own the zonal layer. NXP is not entering an empty field. Infineon, the automotive semiconductor share leader, closed its $2.5 billion all-cash acquisition of Marvell's Brightlane automotive Ethernet business in August 2025 (per Marvell's SEC filing and Infineon disclosures), a deal that strengthens a direct rival precisely at the in-vehicle networking layer where NXP fields its SJA1110 TSN portfolio. The open question on that front is one of cadence. Owning the Brightlane IP is not the same as shipping a unified zonal story, and the assets now sit inside a newly formed Ethernet Solutions line, so the contest may turn on whether Infineon pairs that networking IP with its own microcontrollers and a determinism layer to match what NXP is bundling, or competes one component at a time. Because automotive sockets are typically locked years ahead of production, the window to convert acquired assets into integrated wins is narrower than the deal size suggests.

Renesas, STMicroelectronics, and Texas Instruments anchor the same OEM design cycles, while Qualcomm and NVIDIA press inwards from the high-compute cockpit and ADAS side. While those last two are big names, we would resist reading that high-compute push as a threat to the deterministic layer. Safety-critical, latency-sensitive functions resist full centralization because they require failure isolation and guaranteed timing at the edge of the network. That edge is precisely the zonal layer this solution addresses, so those central compute roadmaps appear complementary to deterministic zonal networking rather than substitutive. A central compute brain still depends on a predictable nervous system to sense and actuate. A different pressure comes from China, where local-content expectations in the world's largest vehicle market are pulling design wins toward domestic suppliers and compressing pricing for global incumbents. That move is intended by the Chinese government to fund home-grown entrants climbing from cockpit and ADAS silicon toward the zonal layer over time. The durable moat for the global suppliers is functional-safety qualification, long validation histories, and mature software ecosystems. That moat is deep, so we expect substitution to likely be gradual rather than abrupt. The structural risk worth watching is bifurcation, where a China stack diverges from a rest-of-world stack and complicates the single, scalable platform thesis at the heart of this announcement.

Against all of this, NXP's response is notable for avoiding the temptation to out-acquire Infineon at the component level. It is an attempt to out-integrate, by selling validated timing as the deliverable. The Quanta selection reinforces the point. A contract manufacturer steeped in hyperscale server assembly entering automotive zonal integration suggests the "server-ization" of the vehicle, where data center build, validation, and CI/CD discipline migrate into the car. Quanta's Asian manufacturing footprint cuts both ways, offering proximity to the China market while exposing the partnership to the same localization currents. For OEMs wrestling with the integration complexity that has stalled several flagship SDV programs, a turnkey determinism platform is a credible procurement argument. The open question is whether automakers, long accustomed to owning system integration, will cede that layer to a silicon-plus-ODM pairing or treat it as a reference to negotiate against.

Looking Ahead

Based on what we are observing, it seems likely that the next phase of the zonal contest will be won at the integration layer, not the transistor. By delivering pre-integrated foundations, NXP is lowering entry barriers for non-traditional players while positioning itself as a system enabler rather than a pure component supplier. This approach not only accelerates time-to-market by several months but also invites a wider ecosystem to build against a common, validated reference architecture. The strategic tell to watch is CoreRide. If NXP can convert this Quanta collaboration into a repeatable reference system with multiple named OEM design wins, it will have done something more durable than ship faster silicon. We will be tracking three signals in particular: whether additional Tier 1s or ODMs slot into the CoreRide ecosystem, whether OEMs accept a supplier-owned determinism layer or insist on owning timing themselves, and how quickly Infineon converts its Brightlane Ethernet assets into integrated design wins. On the first, the caliber and cadence of new CoreRide names will likely tell us more about zonal momentum than headline design-win counts, which can lag the underlying architecture decision by years. The longer-range question is where this class of platform travels next. The primitives underneath it, namely deterministic time-sensitive networking, safe real-time control, and multi-node sensor coordination, are the same primitives a humanoid or industrial robot needs to coordinate many actuators without timing collisions. Recent automotive Ethernet consolidation explicitly flagged robotics as an adjacent demand pool. If NXP and Quanta position the S32 and MotionWise combination as cross-domain rather than automotive-only, the determinism story gains a second growth vector, though robotics volumes remain speculative and safety qualification differs across domains. The deepest question out of all this is structural. If hyperscale manufacturing discipline is genuinely entering the vehicle, the automotive supply chain may start to resemble the data center supply chain. That would be a bigger story than any single design win.

Stephen Sopko | Analyst-in-Residence – Semiconductors & Deep Tech

Stephen Sopko is an Analyst-in-Residence specializing in semiconductors and the deep technologies powering today’s innovation ecosystem. With decades of executive experience spanning Fortune 100, government, and startups, he provides actionable insights by connecting market trends and cutting-edge technologies to business outcomes.

Stephen’s expertise in analyzing the entire buyer’s journey, from technology acquisition to implementation, was refined during his tenure as co-founder and COO of Palisade Compliance, where he helped Fortune 500 clients optimize technology investments. His ability to identify opportunities at the intersection of semiconductors, emerging technologies, and enterprise needs makes him a sought-after advisor to stakeholders navigating complex decisions.